Visa Direct & Push to Card: Your Questions Answered on Fast & Secure B2C Payouts

Looking to streamline your business-to-consumer payouts with speed, security, and ease? You’ve come to the right place. This post is your ultimate, go-to Frequently Asked Questions (FAQ) guide on Visa Direct and Push to Card technologies – the game-changing tools reshaping modern payouts.

In today’s fast-paced world, businesses need payout solutions that are not just fast, but also secure and effortless for recipients. That’s where Visa Direct & Push to Card technologies come in, delivering a powerful, real-time way to disburse funds directly to eligible debit and prepaid cards.

Whether you’re exploring how Visa Direct payouts work, weighing their benefits, or comparing them to other payment methods, especially in the Business-to-Consumer (B2C) space, this blog has you covered. Dive in and discover how these technologies are driving the next evolution of seamless, scalable payouts.

Understanding Visa Direct & Push to Card: Fast and Secure Payment Solutions

What is Visa Direct & Push to Card?

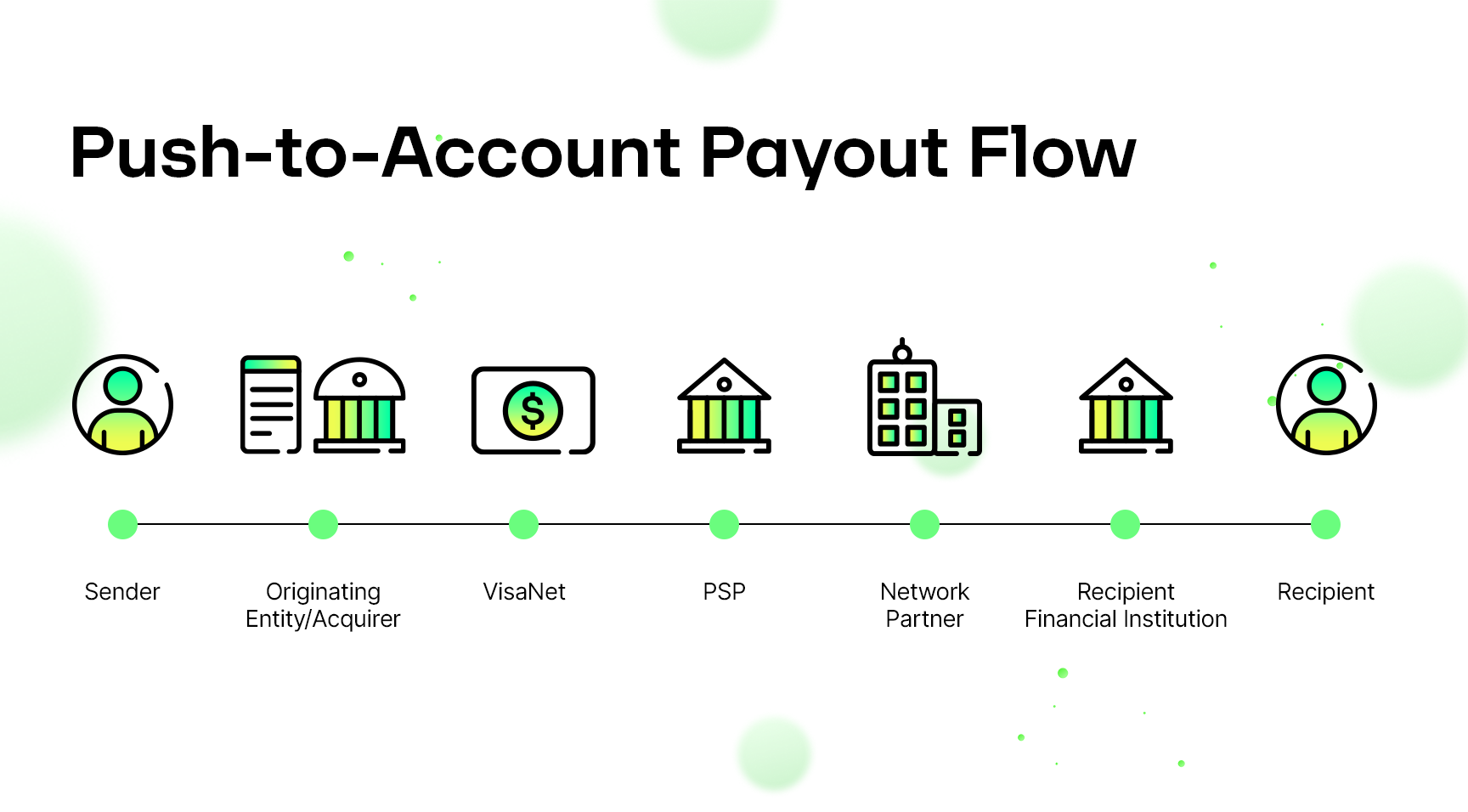

At its core, Visa Direct is a powerful payment network that facilitates near real-time payments globally, leveraging the extensive reach of Visa’s card network. This revolutionary capability is built upon existing Visa functionalities, specifically utilizing Original Credit Transactions (OCTs) – the same infrastructure traditionally used for processing refunds – to enable seamless “push” payments. Visa Direct Push to Card is the underlying technology that enables this next-generation functionality, allowing businesses to send funds directly to an eligible Visa card or other payment credentials. This smart approach bypasses traditional payment routes, often resulting in dramatically faster and more streamlined transactions. For businesses focused on B2C payouts – such as disbursing wages to gig workers or providing refunds to customers – Visa Direct payouts offer a significant advantage, combining speed, efficiency, and ease in one powerful solution.

How do Visa Direct & Push to Card work?

The process begins when a business initiates a payment through a platform or API that integrates with Visa Direct. Using the recipient’s debit card or prepaid card details, the payment request is securely routed through the Visa network. The recipient’s issuing bank then credits the funds to their card, typically within minutes, although the actual fund availability can depend on the receiving bank’s policies. This entire process is underpinned by robust security protocols to ensure the safety of each Visa Direct transaction.

What are the benefits of using Visa Direct for digital payments?

The advantages of using Visa Direct for B2C digital payments are numerous:

- Speed: Recipients often receive funds much faster compared to traditional methods like bank transfers or cheques. Whereas other money movement solutions take time to process, the Visa Direct API enables instant payouts. This instant money transfer capability enhances satisfaction and trust.

- Convenience: Recipients don’t need to perform any additional steps beyond providing their card details to receive funds directly to their familiar debit card. Senders do not need recipient bank account details to send global push payments.

- Security: Visa Direct leverages Visa’s multi-layered security framework, ensuring secure online transactions and protecting sensitive payment information.

- Global Reach: Visa Direct facilitates cross border payments to many countries, making it ideal for businesses with an international reach for payouts.

- Efficiency: Businesses can automate their payout processes through the Visa Direct Payout API, streamlining operations and reducing administrative overhead.

Comparing Visa Direct with Other Payment Methods

How does Visa Direct compare to other digital payment methods?

When comparing Visa Direct to other digital payment methods, several key differences emerge that highlight its unique strengths. Traditional bank transfers can be slower, often taking 1–3 business days for funds to settle – a delay that can impact both business operations and customer satisfaction – compared to the real time payment that Visa Direct Push to Card enables. While Mastercard Send offers a similar “push to card” functionality, Visa Direct benefits from the widespread acceptance of Visa cards globally, giving businesses a broader reach and recipients a more familiar and trusted experience.

.png)

Visa Direct vs. ACH Transfers

Visa Direct payouts stands out from ACH transfers primarily due to its speed. While ACH typically takes 1-3 business days for funds to settle, Visa Direct often enables near real-time or same-day crediting to eligible Visa cards, avoiding long payment processing time offering a significant advantage for time-sensitive payouts. Additionally, Visa Direct leverages the existing Visa card network, allowing for more immediate processing compared to the batch processing system of ACH.

However, ACH transfers generally come with lower transaction fees, making them a cost-effective choice for high-volume, lower-value payouts where speed is not the top priority. ACH is well-suited for recurring payments like payroll, whereas Visa Direct excels in scenarios demanding faster fund availability, such as gig worker payments, refunds, and emergency disbursements.

Visa Direct vs. Wire Transfers

Compared to wire transfers, Visa Direct often provides a faster and potentially less expensive solution, particularly for individual cardholder payouts. Domestic wire transfers can be quick but often involve higher fees, while international wires can be slow and costly due to intermediary banks. Visa Direct can streamline international payouts to eligible cards in participating countries with potentially lower fees and greater convenience.

While wire transfers are often used for high-value transactions and formal business payments, Visa Direct simplifies the process by using the recipient’s debit card details. The integration via the Visa Direct Payout API further enhances efficiency for businesses. This makes Visa Direct a strong contender for faster, more user-friendly B2C disbursements.

Visa Direct vs. Real-Time Payments (RTP)

Both Visa Direct and RTP are designed for speed, aiming for near-instantaneous payment settlement. Visa Direct credits funds to eligible Visa cards rapidly, often within minutes, while RTP settles payments in real-time through a dedicated network. However, Visa Direct benefits from the widespread global acceptance of Visa cards, while RTP adoption is still growing and depends on the participation of financial institutions.

While RTP can support richer data exchange, Visa Direct offers broad reach and convenience for payouts directly to cardholders. For businesses seeking instant money transfer capabilities, both are valuable options, but the best choice depends on the recipient’s access to each network and the specific needs of the payout scenario.

Visa Direct vs. Zelle

Visa Direct and Zelle are both designed for faster payments, but they serve slightly different primary purposes and operate on distinct infrastructures. Zelle is primarily a Peer-to-Peer (P2P) payment network that facilitates direct transfers between bank accounts of enrolled users, often in near real-time. Visa Direct, while also capable of P2P, is particularly powerful for Business-to-Consumer (B2C) payouts directly to eligible debit and prepaid cards, leveraging the extensive Visa card network.

While Zelle relies on users having accounts at participating banks or using the Zelle app, Visa Direct can reach a broader audience with eligible Visa cards, even those not directly linked to a specific Zelle-participating institution. For businesses needing to disburse funds to a wide range of recipients quickly and conveniently, Visa Direct’s “push to card” functionality offers a distinct advantage over Zelle’s bank-to-bank transfer model.

What are the unique features of Visa Direct?

Unique features of Visa Direct include its seamless integration via APIs, its robust security infrastructure built upon Visa’s global network, and its ability to facilitate both domestic and cross-border payments efficiently. The Visa Direct Payout API allows for automated and scalable payout solutions, a crucial aspect for businesses managing numerous transactions.

Why choose Visa Direct over other payment solutions?

Businesses might choose Visa Direct for several compelling reasons:

- Enhanced Recipient Experience: The speed and convenience of receiving funds directly to their card improves recipient satisfaction.

- Reduced Operational Costs: Automation through the API and reduced reliance on manual processes can lower administrative costs.

- Improved Cash Flow Management: Faster payouts can lead to better cash flow management for recipients, especially freelancers and gig workers.

- Global Payout Capabilities: For businesses operating internationally, Visa Direct simplifies fast international transfers.

Security Features of Visa Direct & Push to Card

What security measures are in place for Visa Direct?

Security is paramount with Visa Direct, employing a multi-layered approach to safeguard every transaction. Beyond standard data encryption and sophisticated fraud monitoring systems, Visa Direct leverages the power of tokenization, particularly through the Visa Token Service (VTS). Tokenization replaces sensitive cardholder data, such as the 16-digit Primary Account Number (PAN), with a unique digital identifier called a token. This token is specific to a merchant or even a device, significantly reducing the risk of fraud because the actual card details are never exposed during the transaction process.

The importance of network tokenization, facilitated by VTS, cannot be overstated. Unlike traditional card-on-file storage, where the raw PAN is vulnerable, network tokens offer enhanced security. Even if a token is compromised, it’s rendered useless to fraudsters outside its specific intended use. Furthermore, VTS can automatically update card details associated with a token when a card expires or is replaced, ensuring seamless and secure recurring payments without requiring the user to update their information. This not only bolsters security but also improves the overall payment experience.

How does Visa Direct ensure transaction security?

Visa Direct adheres to strict industry standards and security protocols mandated by Visa. This includes Payment Card Industry Data Security Standard (PCI DSS) compliance for platforms integrating with the API. Each visa direct payout is monitored for suspicious activity, and advanced risk assessment tools are employed to prevent fraudulent transactions.

Are Visa Direct transactions safe for cross-border payments?

Yes, Visa Direct transactions are designed to be secure for cross-border payments. While international transactions may involve additional compliance checks, the underlying security framework remains robust, ensuring the safe transfer of funds across borders.

Use Cases for Small Businesses and Freelancers

How can small businesses benefit from Visa Direct?

Small businesses can leverageVisa Direct for various payout scenarios, such as:

- Paying Suppliers: Making quick and secure payments to vendors.

- Disbursing Refunds: Offering faster refunds to customers, enhancing customer service.

- Paying Gig Workers: Providing timely payments to freelancers and contractors.

What are the advantages for freelancers using Visa Direct?

For freelancers, receiving payments via Visa Direct offers significant advantages:

- Faster Access to Earnings: Unlike traditional invoicing and bank transfer cycles, funds are often available within minutes.

- Convenience: No need to manually deposit cheques or wait for bank transfers to clear.

- Reliability: Direct payouts to their debit card provide a dependable way to receive income.

How does Visa Direct support business transactions?

Visa Direct streamlines business transactions by providing a reliable and efficient method for disbursing funds. The visa direct payout api enables businesses to integrate this capability directly into their existing payment workflows, automating payouts and improving overall efficiency.

How to Set Up and Use Visa Direct for Transactions

What is the process to set up Visa Direct?

Setting up Visa Direct typically involves partnering with a payment service provider (PSP) or platform that offers Visa Direct integration, such as Runa. Businesses will need to go through an onboarding process, which includes verification and setting up their account. Integrating the Visa Direct Payout API into their systems is a key step for automated payouts.

How can users start using Visa Direct for payments?

Recipients don’t directly “sign up” for Visa Direct. Instead, businesses that utilize Visa Direct will send payments to their eligible Visa card. The recipient simply needs to provide their card details to the paying business.

What are the steps to complete a transaction with Visa Direct?

The steps for a business to complete a Visa Direct transaction are generally as follows:

- Initiate Payment: The business initiates a payout through their integrated platform or via the API, specifying the recipient’s card details and the payment amount.

- Secure Transmission: The payment request is securely transmitted through the Visa Direct network.

- Authorization: The recipient’s issuing bank authorizes the transaction.

- Funds Disbursement: The funds are credited to the recipient’s bank account linked to their debit card, often in near real-time.

- Confirmation: Both the sender and receiver may receive confirmation of the completed transaction.

Instant Money Transfer Services: Visa Direct & Push to Card

How does Visa Direct facilitate instant money transfers?

The architecture of the Visa Direct network is designed for speed. By leveraging the existing card rails and streamlining the clearing and settlement processes, it enables near real-time money transfer directly to cards.

What are the benefits of using Visa Direct for remittances?

While Runa focuses on B2C payouts and not P2P remittances, it’s worth noting that the underlying technology of Visa Direct can also be used for remittance services. The benefits include faster delivery of funds to recipients in other countries and potentially lower fees compared to traditional money transfer methods.

How does Visa Direct compare to other instant transfer services?

Compared to other instant money transfer services, Visa Direct benefits from the widespread acceptance of Visa cards and its established global network. While some P2P apps might offer instant transfers within their specific ecosystems, Visa Direct provides a more universal solution for businesses needing to send funds directly to cards.

Visa Direct & Push to Card for Cross-Border Payments

How does Visa Direct handle cross-border transactions?

Visa Direct facilitates cross-border payments by connecting sending and receiving financial institutions across different countries. The network handles currency conversion (if necessary) and ensures compliance with relevant international regulations.

What are the cost benefits of using Visa Direct for international payments?

The cost benefits of using Visa Direct for international payments can include competitive exchange rates and potentially lower transaction fees compared to traditional wire transfers. However, the specific fees can vary depending on the payment service provider and the receiving bank. Businesses should always compare the costs associated with different cross-border payments options.

How secure are cross-border payments with Visa Direct?

Cross-border payments made via Visa Direct benefit from the same robust security measures as domestic transactions. Additional layers of security may be in place to comply with international regulations and to mitigate the risks associated with international fund transfers.

Conclusion

What are the key takeaways about Visa Direct & Push to Card?

Visa Direct & Push to Card technologies represent a significant advancement in payment solutions, particularly for businesses needing to make fast, secure, and convenient B2C payouts. The ability to send funds directly to eligible debit card and prepaid cards in near real-time offers numerous benefits, from enhanced recipient satisfaction to streamlined operational efficiency.

How do Visa Direct & Push to Card integrate into modern payment solutions?

Visa Direct seamlessly integrates into modern payment solutions through APIs, allowing businesses to embed this functionality into their existing platforms and workflows. This integration is crucial for automating payouts and providing a seamless experience for both the sender and the receiver.

What is the future outlook for Visa Direct in the payment industry?

The future outlook for Visa Direct in the payment industry is promising. As the demand for faster and more convenient payment methods continues to grow, Visa Direct is well-positioned to become an increasingly integral part of the digital payments ecosystem, driving innovation and improving the efficiency of B2C transactions globally. For businesses like yours at Runa, leveraging the power of Visa Direct ensures you are at the forefront of providing cutting-edge payout solutions.